A new economic study (also copied below) paints a troubling picture of the potential results a renewed U.S.-China trade war could have on hundreds of thousands of farmers and rural communities, showing American-imposed tariffs would come at a steep cost to U.S. producers while benefiting Brazil and Argentina.

The study, commissioned by the American Soybean Association and the National Corn Growers Association and conducted by the World Agricultural Economic and Environmental Services, shows a new trade war would result in an immediate drop in corn and soy exports to the tune of hundreds of millions of tons. As a result, Brazil and Argentina would claim the lost market share, which would be extremely difficult for American growers to reclaim in the future.

ASA and NCGA both have cautioned against a trade war:

ASA Chief Economist Scott Gerlt said, “The U.S. agriculture sector is going through a significant economic downturn. This work shows that a trade war would easily compound the adverse conditions that are placing financial stress on farmers. Even when a trade war officially ends, the loss of market share can be permanent.”

“The study highlights the dangers that come with broad tariffs on imports,” said NCGA Lead Economist Krista Swanson. “While launching widespread tariffs may seem like an effective tool, they can boomerang and cause unintended consequences. Our first goal should be to avoid unnecessary harm.”

The third-party study comes as U.S. lawmakers and officials from both political parties are increasingly looking at tariff-forward approaches as they work to address troubling Chinese trade practices.

Researchers modeled several scenarios that could play out in a new U.S.-China trade war and found a consistent outcome:

• Severe drop in U.S. exports to China. If China cancels its current waiver (from the 2020 Phase I agreement) and reverts to tariffs already on the books, U.S. soybean exports to China would, according to the study, fall 14 to 16 million metric tons annually, an average decline of 51.8% from baseline levels expected for those years. U.S. corn exports to China would fall about 2.2 million metric tons annually, an average decline of 84.3% from the baseline expectation.

• Brazil and Argentina would benefit. Brazil and Argentina would increase exports and thus gain valuable global market share. Chinese tariffs on soybeans and corn from the U.S.—but not Brazil—would provide incentive for Brazilian farmers to expand production area even more rapidly than baseline growth.

• No place to turn. While it is possible to divert exports to other nations, the study found there is insufficient demand from the rest of the world to offset the major loss of soybean exports to China to support the farmgate value.

The study found a new trade war would lead to a steep drop in soy and corn prices, resulting in a ripple impact across the U.S., particularly in rural economies where farmers live, purchase inputs, use farm and personal services, and purchase household goods.

Leaders at NCGA and ASA believe it is in America’s economic interests to maintain a trading relationship with China, even as both governments work through trade and other concerns. They also noted they support thoughtful consideration of the impacts tariffs and tariff retaliation could have on U.S. farms and rural communities.

Trade Study: How Potential New Tariffs Could Impact U.S. Soybeans and Corn

By Krista Swanson, NCGA Lead Economist • Scott Gerlt, PhD, ASA Chief Economist • Jacquie Holland, ASA Economist

Considerable discussion has surrounded suggestions of ratcheting up tariffs for various reasons on U.S. imports of Chinese products. And experience and research have shown that U.S. agriculture often bears the cost of such trade disputes.

U.S. soybeans and corn are prime targets for tariffs. As the top two export commodities for our country, together they account for about one-fourth of total U.S. agricultural export value. As such, a repeated tariff-based approach to addressing trade with China places a target on both U.S. soybeans and corn. Farmers and rural economies pay the price as a result.

The National Corn Growers Association and American Soybean Association asked World Agricultural Economic and Environmental Services (WAEES) to evaluate the impact a trade war would have on soybeans and corn today. Bottom line: A repeated tariff-based approach accelerates conversion of cropland in South America, which has permanent ramifications on soybean and corn exports worldwide. And U.S. soybean and corn growers bear the burden.

China Trade War Background

U.S. lawmakers from both parties are increasingly concerned with several Chinese trade practices. While addressing unfair trade practices is warranted, the use of import tariffs as a method to address trade concerns negatively impacts the U.S. farmer and has ramifications for the U.S. economy. In the 2018 trade war, the U.S. extended tariffs on steel and aluminum to several major trading partners and separately imposed tariffs on an extensive range of imported products from China. In response, China and other nations imposed retaliatory tariffs on numerous U.S. products, including many agricultural and food products. This led to significant reduction in U.S. agricultural exports to those nations. As a result of retaliatory tariffs from the onset in summer 2018 through the end of 2019, U.S. agricultural export losses exceeded $27 billion, with China accounting for about 95% of the value lost (USDA).

China and the U.S. signed a “Phase I Agreement” in January 2020, which helped end the trade war. Part of the agreement stipulated China would purchase $80 billion of U.S. agricultural products over 2020 and 2021. China dramatically increased its purchases of U.S. agriculture products during that time, though final volumes fell short of those obligations, with only $59.2 billion of U.S. agricultural products purchased by China. Logistics issues stemming from the COVID-19 pandemic and resulting global supply chain crisis further limited China’s purchases, but the revival in trade, which included record volumes of soybeans and corn, helped repair goodwill between China and the United States.

U.S. farmers have worked more than 40 years to establish and nurture their strong trade relationships with China. During those decades, many farmers visited China as part of trade teams, and Chinese buyers visited the United States. The 2018 trade war created concerns about the reliability of U.S. supply creating an incentive for China to invest in alternative supply chains. These investments encouraged irreversible production area expansion in U.S. agricultural competitor nations. While it took decades to fully develop trade with China, the trade war quickly reversed many years of efforts in ways that remain difficult to recover.

While the 2018 trade war with China is a recent reference point, there are additional historical examples of nations targeting U.S. agriculture with retaliatory measures given agriculture’s importance as an industry, its reliance on trade, and historical political influence (farmdoc). As the largest exporter of agricultural products in the world (WTO), the U.S. exports about 20% of its total agricultural production (USDA).

Among all U.S. agricultural products, soybeans and corn are prime targets: As mentioned above, these crops are the top two commodities contributing to the U.S. agricultural export value, accounting for about one-fourth of the total (USDA). Intermediate products from the two commodities, such as soybean meal and oil, ethanol and distillers grains, capture additional share of that total.

Study Framework

The purpose of the study is to investigate the impacts of another potential U.S. and China trade war in which China responds to U.S. punitive tariffs by imposing retaliatory tariffs on corn, soybeans, and soybean products (meal and oil), as would be expected given the 2018 trade war and overall historical precedent.

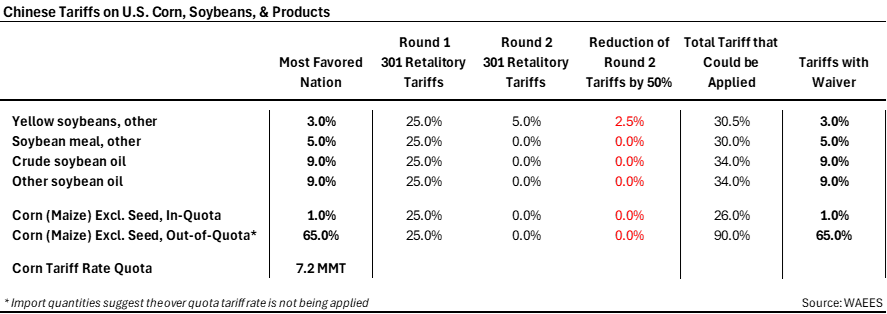

Many of the tariffs China imposed on U.S. agricultural products from the 2018 trade war remain in place but have been granted a waiver that has been renewed annually. These tariffs could easily be reinstated by China. The table below shows the varying levels of Chinese tariffs on U.S. products, including the base most favored nation (MFN) status and the rounds of retaliatory tariffs and partial reduction that sum to the total tariff that could be applied.

With the waiver process China has been implementing thus far, the rate that has been applied is the “tariffs with waiver” column, equal to the most favored nation rate. China still has an MFN tariff rate quota (TRQ) set at 7.2 million metric tons for corn. Despite corn imports significantly above that level, China has indicated no changes will be made but also has not been enforcing it. Importantly, China can restrict imports at any time without public disclosure, including by enforcing or changing the administration of its TRQ.

To evaluate how a trade war could impact U.S. soybeans and corn over the next decade, WAEES evaluated possible scenarios. One approach was the assumption that China would apply the rate from the “Total Tariff that Could be Applied” column to imports of U.S. corn, soybeans, and soybean products. Another approach is the assumption that China would apply a 60% tariff to imports of U.S. corn, soybeans, and soybean products if a 60% tariff on Chinese goods was imposed by the United States.

In both cases, the tariffs are assumed to begin in 2025 and affect the 2025/26 marketing year, staying in place through the 2035/36 marketing year. Argentina, Brazil, and trading partners in the Rest of the World (ROW) stay at the “Most Favored Naton” tariff rates. China continues to ignore its TRQ so that out-of-quota tariffs do not apply to any country. This analysis does not consider the impact of increased tariffs on input costs for crop production.

A baseline provides a starting point for the analysis with a forecast for prices and quantities of soybeans and corn over the next 10 years based on current policy, which is the tariff waivers by China. The tariff scenarios are compared against the baseline to evaluate their effects.

Study Findings

U.S. Soybean & Corn Exports Drop While Brazil Gains Market Share

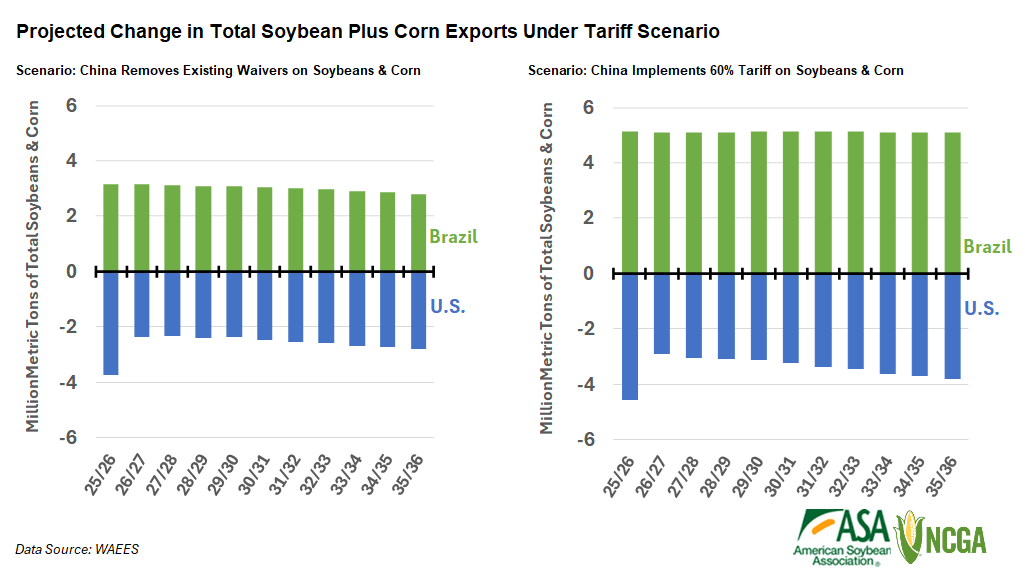

If China cancels its waiver and reverts to tariffs already on the books, U.S. soybean exports to China fall between 14 and 16 million metric tons annually, an average decline of 51.8% from baseline levels expected for those years. U.S. corn exports to China fall about 2.2 million metric tons annually, an average decline of 84.3% from the baseline expectation. Although the export quantity decline is much lower for corn than soybeans, reflecting the smaller quantity of corn exported to China, the relative change from the baseline quantity is significant for corn.

While it’s possible to divert exports to other nations, there is not enough demand from the rest of the world to offset the major loss of soybean exports to China. At the same time, Brazil and Argentina gain global market share with increased exports. The U.S. loses a combined total of 2.3 to 3.7 million metric tons of soybean plus corn exports annually, while Brazil gains an average of 4.6 million metric tons of soybean plus corn exports annually.

Chinese tariffs on soybeans and corn from the U.S. but not Brazil provide incentive for Brazilian farmers to expand production area even more rapidly than baseline growth. The expansion is magnified because some land area in Brazil can be used to grow a soybean and corn crop in the same year. Land transitioned into production area in Brazil will remain in production. The impact on U.S. soybean and corn farmers isn’t limited to a short-term price shock: This is a long-lasting ramification that changes the global supply structure.

A 60% retaliatory tariff level intensifies the shock, resulting in a loss of over 25 million metric tons of soybean exports to China and nearly 90% of corn exports to China. In this situation, the U.S. loses a combined total of 2.9 to 4.6 million metric tons of soybean plus corn exports annually, while Brazil gains an average of 8.9 million metric tons of annual soybean plus corn exports over the projection timeline.

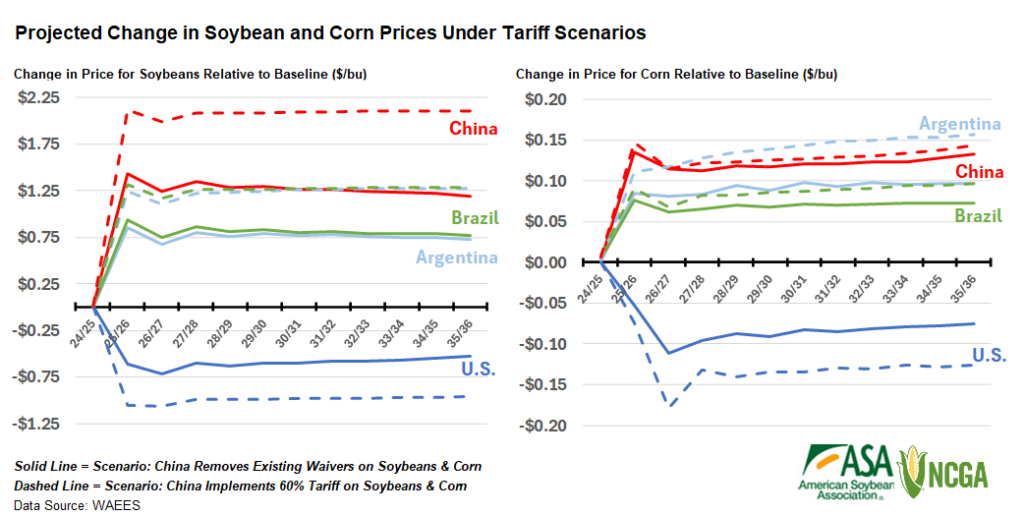

U.S. Soybean & Corn Prices Drop from Already Low Levels, Brazil Benefits

A removal of the waiver on existing tariff levels results in a U.S. soybean price that is $0.60 per bushel below the baseline, on average, over the forecast horizon. The price rises for farmers in Brazil and Argentina, capturing more than $0.75 per bushel over the baseline price on average. In China, the price rises to $1.27 above baseline, on average. The price increases in China make imports more expensive for China but are beneficial to its farmers. The result is China buys less foreign soybeans and corn while alternatively expanding its domestic production area for both crops and retaining the added economic value of the higher price.

The U.S. corn price drops $0.08 per bushel below baseline, on average, while farmers in Argentina and Brazil capture a nearly equivalent increase in their corn price. In China, the price of corn rises $0.12 per bushel, on average.

Under a 60% tariff scenario, the price for U.S. soybeans falls nearly $1 per bushel on average, and the price for U.S. corn drops $0.13 per bushel, on average, from already low baseline price levels. While U.S. soybean and corn farmers are hit harder, farmers in Argentia, Brazil, and China see even greater increases in their prices for soybeans and corn.

Comparative prices in Argentina and Brazil rise while farmers in those nations benefit from a combination of higher prices and expanded export opportunity. Alternatively, U.S. farmers face further price declines at a time when costs remain at record levels and commodity prices are already declining. Current USDA projections for 2023 and 2024 net cash income would result in the largest two-year decline since the 1970s, leaving U.S. farmers exceptionally vulnerable to the adverse impacts of trade war in 2025.

U.S. Soybeans & Corn Lose Production Value, Rural Economies Suffer

Depending on the scenario, U.S. soybeans lose an average of 1.3 to 2.2 million acres annually over the forecast horizon. U.S. corn gains an average of 0.2 to 0.5 million acres annually depending on scenario, but this is not a “win” for U.S. corn.

The gain in corn acres does not offset the loss in soybean acres: This is collectively a loss for U.S. soybean and corn production and numerous farmers growing both crops. Meanwhile, other nations expand total soybean and corn production area. For example, growth in combined production area in Brazil is nearly equivalent to the combined loss in the United States. China also gains acres.

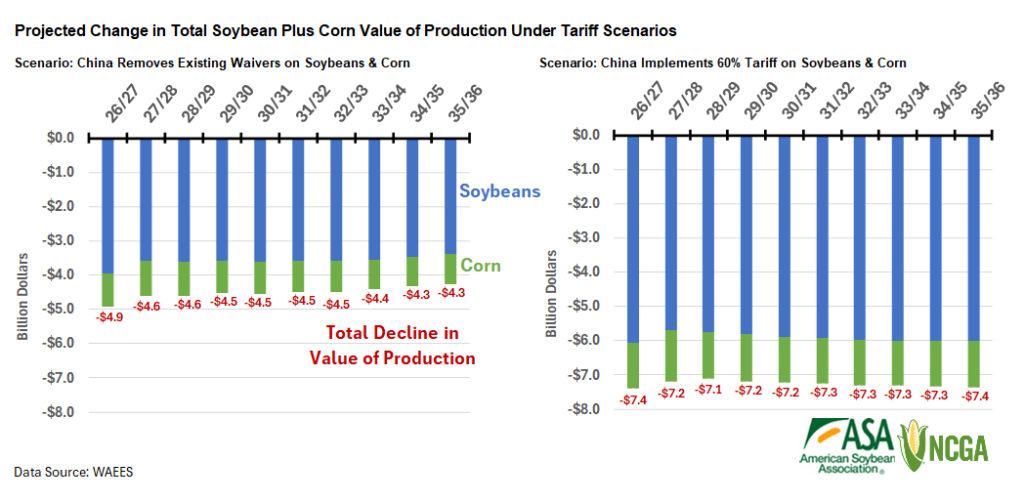

Depending on the scenario, U.S. soybean farmers lose an average of $3.6 to $5.9 billion in annual production value. U.S. corn farmers lose an average of $0.9 to $1.4 billion in annual production value, as the resulting decline in corn prices more than offsets the acreage change.

This burden is not limited to the U.S. soybean and corn farmers who lose market share and production value. There is a ripple impact across the U.S., particularly in rural economies where farmers live, purchase inputs, utilize farm and personal services, and purchase household goods.

U.S. soybean and corn farmers and businesses connected to growing these crops make significant contributions to the U.S. economy. When U.S. soybean and corn acres are lost, the impact ripples throughout U.S. communities. The baseline and scenario results from the WAEES study were used to estimate economic impact using IMPLAN, a regional economic analysis software and data application.

The combined soybean and corn contribution to total economic output could be expected to drop $4.9 billion annually under the first scenario or $7.9 billion annually under the second scenario. Among the sectors heavily affected by the soybean and corn scenarios are manufacturing and mining of crop protection, fertilizer products, and energy products, as well as real estate and transportation.

In line with the WAEES study approach, which did not consider the impact of increased tariffs on input costs for crop production, costs were held constant in the economic impact analysis, as was the number of farmers. If a renewed trade war impacts inputs, the economic impact results would be even more stark, particularly given the heavy reliance of the soybean and corn sectors on inputs such as crop protection products and fertilizers. Although not modeled, a trade war revival in an already challenging time for farm income would likely expedite loss of farms and employment throughout the industry.

Conclusion

Our results confirm Chinese tariffs on U.S. agriculture can have a damaging effect with permanent consequences that extend far beyond a short-term price drop. Another recent study evaluates a potential wider agriculture sector trade war using different baseline assumptions on response elasticities and tariff levels, resulting in even more detrimental impacts to U.S. farmers.

Regardless of approach and assumptions that determine the severity of the modeled outcome, the overarching consequences are the same. While dollar value impacts can represent losses in export value or value of production, neither study can account for the permanent implications from the loss of the United States’ reputation with trading partners, as evident in the fact that U.S. agriculture today is still rebuilding from the 2018 trade war. Further, these studies do not measure the accelerated transition of new production areas in South America, which will remain in use long after a trade war.

A reignited trade war would reduce both U.S. soybean and corn prices and the combined production area of the two crops. If it were to occur, a trade war would not only reduce the value of production for U.S. farmers but also have a ripple effect throughout the U.S. economy. Meanwhile, farmers in Argentina and Brazil would see higher soybean and corn prices and be poised to more rapidly expand their production areas. The economies of these two countries would benefit from rising production value. In short, South America would gain on all fronts at the expense of U.S. farmers and the U.S. economy.

Comments