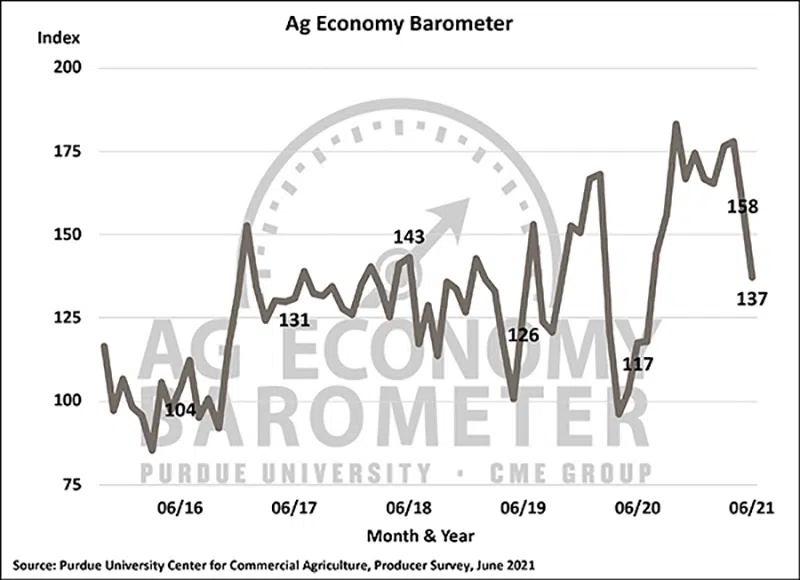

The Purdue University/CME Group Ag Economy Barometer marks a second month of sharp declines, down 21 points to a reading of 137 in June. Producers were less optimistic about both current conditions on their farming operations as well as their expectations for the future. The Index of Current Conditions dropped 29 points to a reading of 149, and the Index of Future Expectations fell 17 points to a reading of 132. The Ag Economy Barometer is calculated each month from 400 U.S. agricultural producers’ responses to a telephone survey. This month’s survey was conducted June 21-25.

“Farmers expect their input costs to rise much more rapidly in the year ahead than they have over the last decade, contributing to their concerns about their farm finances and financial future,” said James Mintert, the barometer’s principal investigator and director of Purdue University’s Center for Commercial Agriculture.

Since peaking in April, producers’ view of their farms’ financial performance has fallen sharply. The Farm Financial Performance Index, which is based on a question that asks producers about expectations for their farm’s financial performance this year compared to last year, declined 30 points this month, and 42 points since April, to a reading of 96.

Weakening perceptions of farm financial performance spilled over into the Farm Capital Investment Index, which declined 11 points to a reading of 54, the lowest investment index reading since May 2020. The decline in the investment index appears to be driven more by plans to hold back on constructing new farm buildings and grain bins than purchasing farm machinery. In June, 61% of producers said they reduced plans for new construction, while 9% said they increased plans. In comparison, 44% of producers indicated they plan to reduce their machinery purchases, 45% plan to hold purchases constant, and 10% plan to increase purchases, all compared to a year ago.

Rapidly rising production costs related to both consumer and farm input price inflation are a concern for agricultural producers. Nearly 30% of producers said they expect farm input prices to rise by 8% or more in the upcoming year, which would be more than four times the average rise over the last 10 years of just 1.8%.

On the other hand, 21% of producers expect prices paid for inputs to increase less than 2%, which would be more in line with recent history. Interestingly, producers expect farm input costs to rise more rapidly than prices for consumer items, which could pressure their margins. For example, just 17% of respondents said they expect consumer prices to rise by 8% or more over the next year.

Labor concerns may also be contributing to producers’ anxiety as farms that normally hire nonfamily labor reported more difficulty in hiring labor this year than in 2020. Just over half (54% in 2020, 51% in 2021) of those surveyed reported hiring nonfamily members. In June 2021, nearly two-thirds (66%) of respondents said they either had “some” or “a lot of difficulty” in hiring adequate labor, that compared to just three out of 10 respondents in 2020.

Even as sentiment dipped in June, producers remained bullish on farmland values. The Short-Term Farmland Value Expectations Index, based upon producers’ 12-month expectation for farmland values, declined nine points to a reading of 148; however, that matches the third-highest reading for the index since data collection began in 2015. The Long-Term Farmland Value Expectations Index, based upon producers’ five-year outlook, declined just 3 points to a reading of 155, which was also the third-highest reading on record for that index.

Corn and soybean producers gave a somewhat mixed response when asked about their expectations for cash rental rates in 2022. In May, nearly two-thirds of producers said they expected rates to rise in 2022 compared to 2021; however, in June less than half (47%) of corn-soybean producers said they expect rental rates to rise in the coming year. Among those who expect rates to increase, many anticipate the rise will be significant. Nearly half expect cash rental rates to rise between five to less than 10% and nearly one-third expect rates to rise by 10% or more.

Interest in leasing farmland for solar energy projects has risen sharply over the last couple of years. Nearly one-third (32%) of farms in the June survey said they are aware of solar leasing opportunities for their farmland. Of those aware of leasing opportunities, 29% of them said they had engaged in discussions with companies about leasing some of their farmland. Less than 3% (2.6%) of all survey respondents reported having signed a solar lease on some of their farmland. This is approximately double the percentage of producers who reported having signed a carbon sequestration contract on barometer surveys conducted this past winter and spring.

Read the full Ag Economy Barometer report. The site also offers additional resources – such as past reports, charts and survey methodology – and a form to sign up for monthly barometer email updates and webinars.

Each month, the Purdue Center for Commercial Agriculture provides a short video analysis of the barometer results. For even more information, check out the Purdue Commercial AgCast podcast. It includes a detailed breakdown of each month’s barometer, in addition to a discussion of recent agricultural news that affects farmers.

Ag Economy Barometer falls for second month; rising input costs causing concern for farmers. (Purdue/CME Group Ag Economy Barometer/James Mintert)

Comments